For families interested in protecting their assets, reducing or avoiding the estate tax entirely, and otherwise building generational wealth, trusts have long been the vehicle of choice for the world’s wealthiest families.

But the power of trusts isn’t limited to the ultra wealthy. Everyday families can make use of something called blind trusts to not only pass on their wealth, but set an expectation of how that wealth will be managed (and protected) for generations to come.

Today, we reveal what a blind trust is, how it works, and how you can set one up for yourself.

Before we dive into the complex world of blind trusts, let’s define a few key terms.

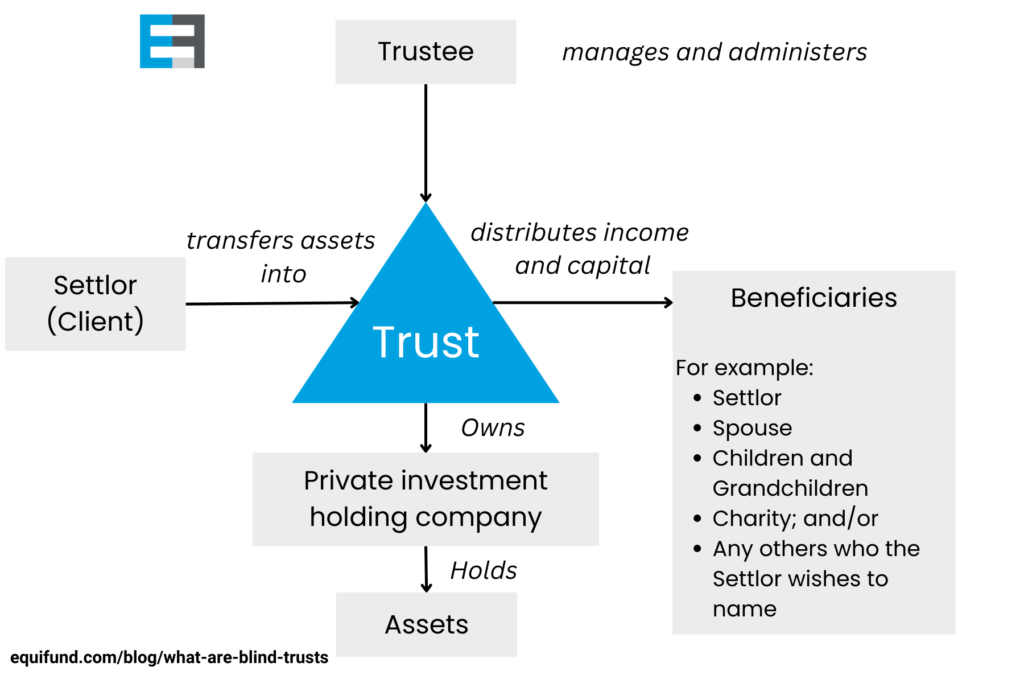

Grantor or Trustor: The person or entity who establishes a blind trust. They are the ones who transfer their assets into the trust, relinquishing control and ownership.

Trustee: The party responsible for managing the blind trust’s assets and making investment decisions on behalf of the grantor. This can be an individual or a financial institution with the necessary expertise and fiduciary duty to act in the best financial interests of the grantor and the beneficiaries.

Grantee or Beneficiary: The individual or organization designated to receive the assets or distributions from the blind trust. They have a beneficial interest in the trust, but do not have control over its management. In some cases, the beneficiary can be the same person as the trustor. But in other cases, the beneficiary is one of the trustor’s loved ones.

A blind trust is a powerful financial tool that individuals, including business leaders and government officials, often utilize to mitigate any conflict of interest between their personal investments and professional roles.

In brief, it’s a trust established where the owner, known as the trustor, relinquishes full control and management of the trust’s assets to an independent party called the trustee. The trustee is entrusted with the authority to handle the assets and make investment decisions without the trustor’s knowledge or consent, hence the term “blind.”

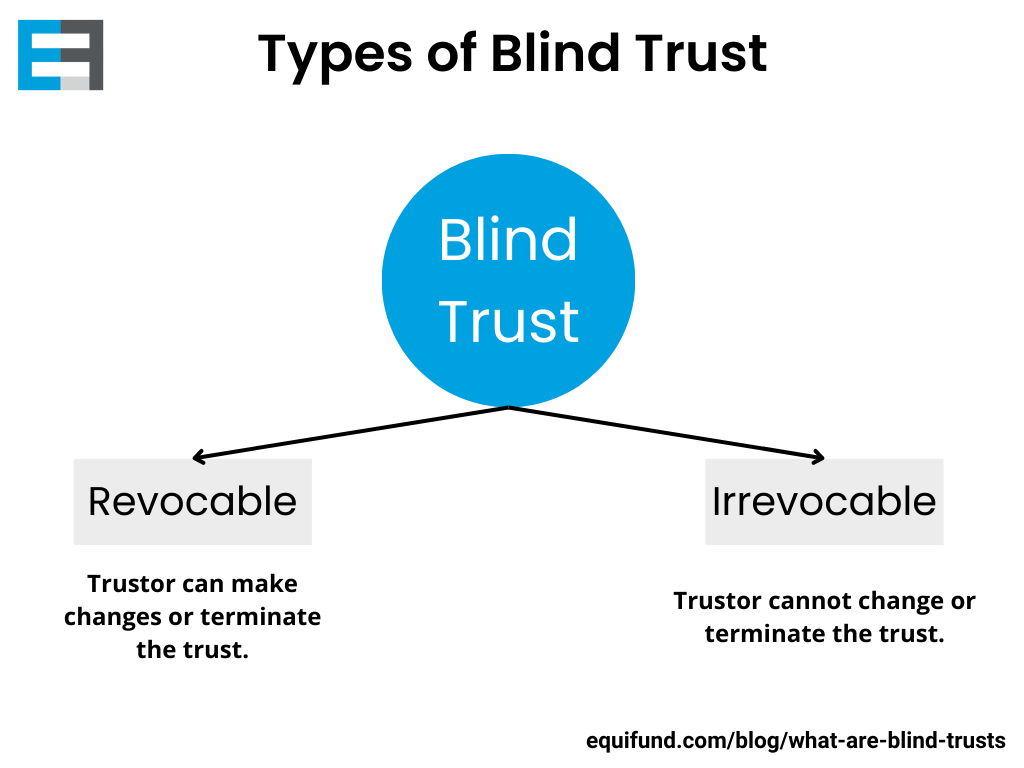

The trustee’s role is crucial in maintaining privacy and preventing real or perceived conflicts, ensuring that the trustor remains uninformed about the trust’s holdings and the impact of their official actions on their private interests. Blind trusts can also be sub-categorized as either a revocable trust or an irrevocable trust. The main difference being whether or not the trustor’s can make changes to the trust.

Overall, blind trusts empower individuals to separate their wealth from their decision-making, fostering transparency and integrity in both personal and professional realms.

Here’s a table that shows you the rules around blind trusts in each U.S. state. It also covers D.C., the Virgin Islands, Guam, and Puerto Rico.

The primary distinction between a trust and a blind trust lies in the level of information and control accessible to the trustor and beneficiary.

A trust is a legal arrangement where the trustor (the wealthy individual creating the trust) places financial holdings under the control of a trustee for the benefit of a beneficiary. In a regular trust, the trustor maintains control over the assets and can make decisions regarding how they are invested and distributed to the beneficiary. The beneficiary is also aware of the assets within the trust.

A blind trust, on the other hand, operates differently. In this type of trust, the trustor and beneficiary do not have access to or knowledge of the trust’s investment holdings.

In this fiduciary relationship, the trustee has complete control over managing the investments, and the trustor and beneficiary have no say in this matter whatsoever.

The lack of transparency in a blind trust is deliberately designed to prevent any conflict of interest and maintain the privacy of the trust’s assets. A corporate executive, for example, can place shares of their company’s stock in a blind trust to avoid insider trading accusations.

So while a trust offers control and transparency, allowing the trustor to make decisions about asset management, a blind trust restricts access and knowledge, giving full control to the trustee to prevent conflicts of interest and safeguard the privacy of the trust’s assets.

Overall, blind trusts provide a strategic solution for individuals seeking to separate their personal investments from their professional obligations.

By entrusting an independent trustee with full control over assets and investments, trustors can avoid potential conflicts of interest with greater transparency, while enjoying privacy and the freedom to focus on their responsibilities without undue influence.

Let’s break down the key benefits of a blind trust:

Asset Protection

By placing assets into a blind trust, individuals can shield themselves from potential conflicts of interest that may arise due to their employment or public office. For example, a legislator could establish a blind trust to separate their personal financial interests from their official actions, ensuring impartial decision-making.

Trustee Discretion

In a blind trust, the trustee enjoys complete discretion over managing the trust assets and any income generated within the trust. They can buy, sell, or modify investments without needing to disclose these transactions to the trustor, thereby reducing the risk of bias or favoritism.

Impartiality

A crucial element of a blind trust is the appointment of an independent trustee who does not have a close personal relationship with the trustor. This impartial third party ensures that the trust operates objectively and avoids conflicts of interest.

Privacy

Blind trusts offer a high level of privacy since the trustor has no knowledge of the trust’s contents or the trustee’s investment decisions. This confidentiality helps protect the trustor’s financial information and prevents potential external influences on decision-making.

Flexibility

Blind trusts can be either revocable or irrevocable. A revocable trust allows the trustor to make changes or terminate the trust if circumstances change, while an irrevocable trust provides a more permanent structure for asset management.

One benefit of the latter is that irrevocable trusts are not taxed as an asset, meaning it can be leveraged to reduce tax liability. Another tax reduction tool savvy investors use is a self-directed IRA LLC .

While you don’t have direct control over a blind trust, you can still structure in a way where it allocates capital according to your wishes. For example, you can instruct your trust to give conditional gifts (i.e. I give a car to my son once he passed his driver’s exam).

Setting up a blind trust can serve various purposes, primarily aimed at avoiding conflicts of interest and maintaining objectivity in specific positions or situations. Here are a few examples of the types of individuals who opt for blind trusts.

Corporate Executive

Blind trusts are frequently used by corporate executives or board members. Those who hold substantial shares in the company and have access to privileged information may find trading restrictions a hindrance to effectively managing their investment portfolio. Such regulations can be sidestepped if the executive’s assets are moved into a blind trust.

Retired Businessman

Consider a retired businessman who has a desire to pass on his wealth to future generations or charitable causes. Establishing a blind trust allows him to plan for the seamless transfer of assets without any disruptions. The trust can outline specific instructions for the management and distribution of the trust assets, ensuring a smooth transition and potentially providing financial security for his heirs or philanthropic endeavors.

Public Servants

Public servants, such as government officials, may utilize blind trusts to manage private sector assets owned by themselves, their spouses, and dependent children. This practice becomes essential when their involvement in legislation or decision-making could potentially impact their investments. Placing assets in a blind trust, particularly an irrevocable one, ensures that these elected officials can act impartially and avoid public scrutiny around their holdings.

Religious Figures

Religious individuals may employ blind trusts to handle assets received from their parishioners. By utilizing a blind trust, they can maintain privacy and conceal the specific assets they receive, ensuring transparency and avoiding conflicts of interest within their religious duties.

Wealthy Individuals with Sudden Windfalls

Individuals who unexpectedly come into large sums of money, such as inheritances, lottery winnings, or gambling proceeds, may choose to establish a blind trust for privacy and conflict avoidance.

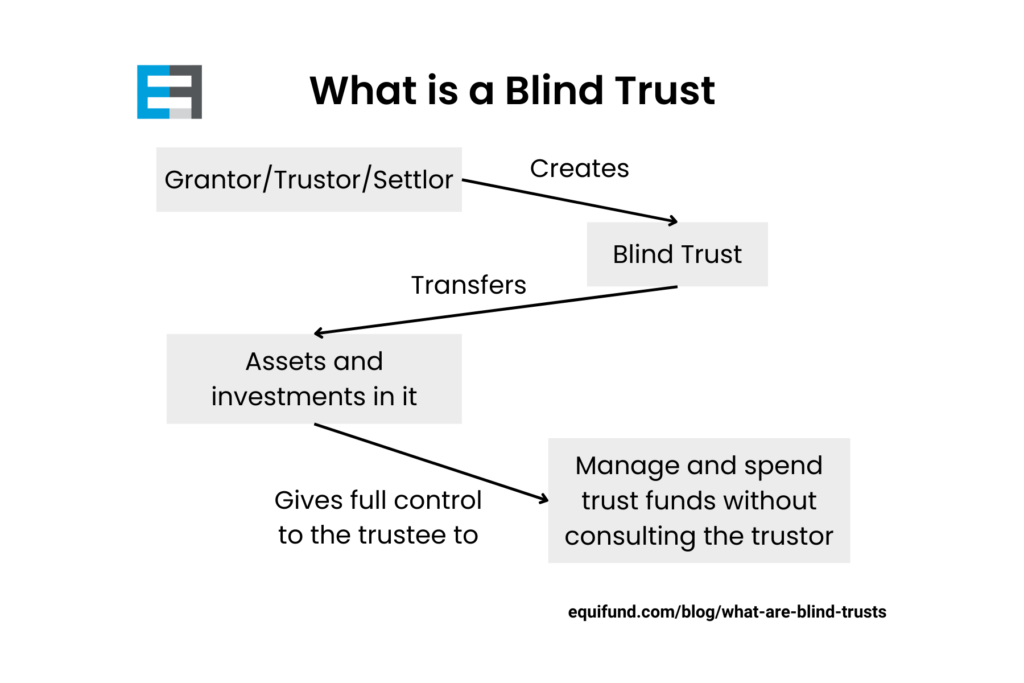

At a high level, a blind trust is a legal arrangement in which a person places their assets or investments under the control of a trustee.

Once the grantor has set up the trust and assets are transferred, the grantor no longer has control over or knowledge of the specific assets held in the trust. From here on out, the trustee manages the assets held in the blind trust. The trustee has the authority to make investment decisions, buy or sell assets, and take other actions in accordance with the trust agreement.

The grantor typically provides general guidelines regarding investment strategies but does not have involvement in day-to-day investment decisions.

And while the grantor remains unaware of the trust’s specific activities, they may receive periodic reports from the trustee that disclose the trust’s overall performance, such as financial statements or summaries. These reports typically provide aggregate information without disclosing individual holdings.

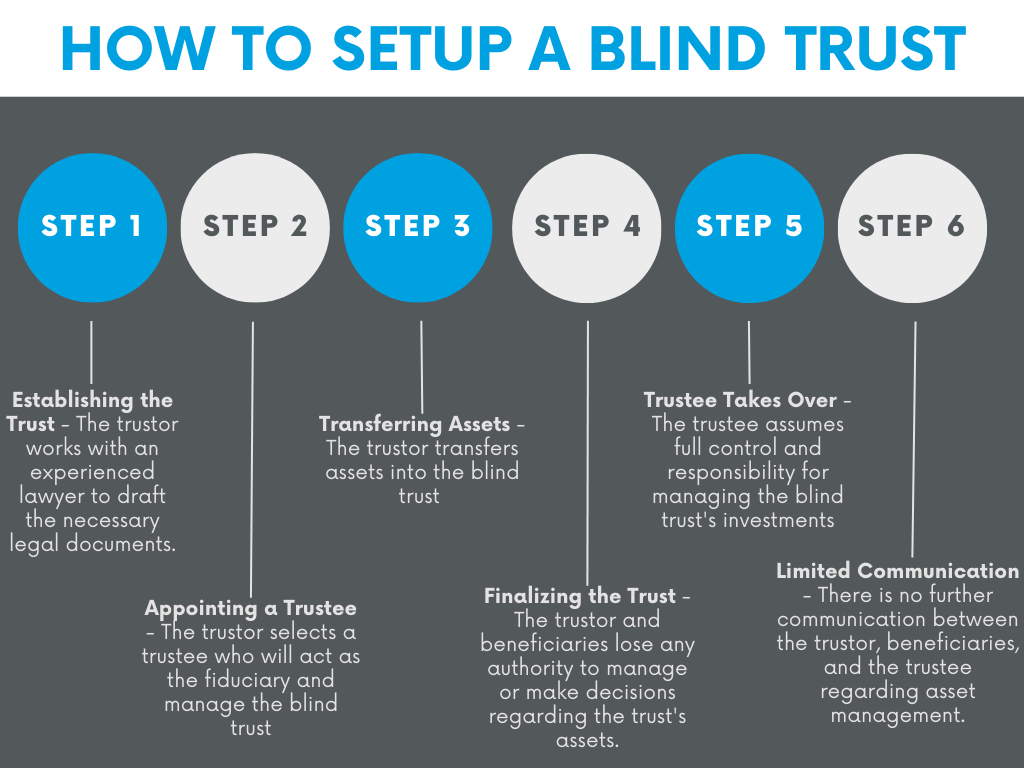

In the realm of financial planning and asset management, a blind trust stands as a unique and distinct entity—offering a heightened level of confidentiality and hands-off management. Let’s break down the process of setting up and running a blind trust.

The trustor, also known as the originator, initiates the process of setting up a blind trust. They work with an experienced lawyer to draft the necessary legal documents for the trust, including the trust instrument. The trustor may specify the beneficiaries and outline investment goals during this stage.

A blind trust can be either revocable or irrevocable, depending on the trustor’s goals. A revocable trust allows the trustor to make changes to the trust, including modifying beneficiaries or replacing the trustee. In contrast, an irrevocable trust cannot be changed once established and provides additional asset protection, making it harder for creditors or government entities to claim the assets.

The trustor selects a trustee who will act as the fiduciary and manage the blind trust. It is crucial to choose a trustee who is both trustworthy and knowledgeable in investments. It is recommended to select someone independent, without a close personal relationship, such as a friend or relative, to avoid conflicts of interest.

The trustor transfers assets, such as funds, equities, bonds, or real estate, into the blind trust. These assets become part of the trust property, and the trustor no longer has direct control over them.

Once the trust is established and assets are transferred, the trustor signs the necessary documents, completing the formation of the blind trust. At this point, the trustor and beneficiaries lose any authority to manage or make decisions regarding the trust’s assets.

The trustee assumes full control and responsibility for managing the blind trust’s investments. They have the full discretion to make decisions about buying, selling, or trading securities within the trust. The trustor and beneficiaries have no involvement or knowledge of these investment activities.

Following the establishment of the blind trust, there is no further communication between the trustor, beneficiaries, and the trustee regarding asset management. The trustee operates independently, ensuring that the trust’s assets are handled in accordance with the trust agreement and applicable laws.

The exact details and requirements of a blind trust can vary depending on jurisdiction and specific circumstances, so it is important to consult with legal professionals familiar with applicable laws when setting up such a trust.

With a blind trust, you can effectively manage your wealth while ensuring transparency and protecting your reputation.

Whether you’re a high-profile politician or a lottery winner, a blind trust offers numerous benefits. It establishes a layer of separation that helps eliminate any real or potential conflict of interest and shields you from accusations of wrongdoing. Additionally, it allows individuals who plan to pass their wealth onto future generations to maintain their financial privacy.

At Equifund, we allow you to invest in Private Market deals using your Trusts. To set that up, we must first verify the Trust is in good standing by requesting the following documents:

This article is not an Equifund Crowd Funding Portal Inc communication. It is brought to you by Equifund Technologies, LLC.

All information contained in this communication should not be considered investment advice, but education and entertainment only.Investing in private or early stage offerings (such as Reg A, Reg S, Reg D, or Reg CF) involves a high degree of risk. Securities sold through these offerings are not publicly traded and, therefore, are illiquid. Additionally, investors will receive restricted stock that is subject to holding period requirements. Companies seeking capital through these offerings tend to be in earlier stages of development and have not yet been fully tested in the public marketplace. Investing in private or early stage offerings requires a tolerance for high risk, low liquidity, and a long-term commitment. Investors must be able to afford to lose their entire investment. Such investment products are not FDIC insured, may lose value, and have no bank guarantee.

Hint: Don’t take ANY stock market risk and do THIS instead

Tax liability is the total amount you owe to the government. Discover how to calculate your tax liability, and what you can do to legally pay as little as possible.

An inside look at how I became the Private Capital Insider

By submitting your email address you will receive access to this report and a free subscription to Equifund’s private investment newsletter. You can unsubscribe at any time and read more about our privacy policy here.

Proprietary devices that could revolutionize spinal surgery and greatly improve success rates, reduce pain, and lower costs.

Over 20 patents have been issued to protect the company's technologies. Just received FDA clearance for their next-generation KG2 spinal fusion technology.30 N Gould St, Ste R

Sheridan, WY

82801

Equifund.com (the “Site”) is owned and maintained by Equifund Technologies, LLC, which is neither a registered broker-dealer, investment advisor nor funding portal. All securities listed here are being offered by, and all information included on this Site is the responsibility of, the applicable issuer of such securities. The intermediary facilitating the offering will be identified in such offering’s documentation.

Any broker-dealer related securities activity are conducted only by regulated entities that are identified in the offering documentation for the given offering. In the case of offerings of securities under Regulation Crowdfunding, Equifund Crowd Funding Portal Inc., a funding portal which is registered here with the US Securities and Exchange Commission (SEC) as a funding portal and is a member of the Financial Industry Regulatory Authority (FINRA), acts as intermediary for the offering.

Certain pages discussing the mechanics and providing educational materials regarding regulation crowdfunding offerings may refer to Equifund Technologies, LLC and Equifund Crowd Funding Portal Inc. collectively as “Equifund”, solely for explanatory purposes.

Investment opportunities posted and accessible through the site are of three types:

The first type is Regulation Crowdfunding offerings (JOBS Act Title III), which are offered to non-accredited and accredited investors alike. These offerings are made through Equifund Crowd Funding Portal Inc. The second type is Regulation A offerings (JOBS Act Title IV; known as Regulation A+), which are offered to non-accredited and accredited investors alike. These offerings are published through Equifund Technologies, LLC (unless otherwise indicated). The third type is Regulation D, Rule 506(c) offerings, which are offered only to verified accredited investors. These offerings are published through Equifund Technologies, LLC (unless otherwise indicated).

Any securities offered on this website have not been recommended or approved by any federal or state securities commission or regulatory authority. Equifund and its affiliates do not provide any investment advice or recommendation and do not provide any legal or tax advice with respect to any securities. All securities listed on this site are being offered by, and all information included on this site is the responsibility of, the applicable issuer of such securities. Equifund does not verify the adequacy, accuracy or completeness of any information. Neither Equifund nor any of its officers, directors, agents and employees makes any warranty, express or implied, of any kind whatsoever related to the adequacy, accuracy, or completeness of any information on this site or the use of information on this site.

By accessing this site and any pages on this site, you agree to be bound by our Terms of Use and Privacy Policy, as may be amended from time to time without notice or liability.

You can learn more about investing in crowdfunding from the SEC, FINRA or NASAA.

Additional information about companies raising money is also available on the SEC’s EDGAR Database.

Copyright © 2024 Equifund . All Rights Reserved.